What is a foreign spin-off?

Canadian investors (investor) often own foreign corporation shares in their portfolios. Where a foreign corporation (original corporation) distributes shares of another corporation (spin-off corporation) in kind due to a corporate reorganization, the transaction is commonly referred to as a foreign spin-off. Post reorganization, the investor now owns shares of the original and spin-off corporations in their portfolio.

Generally, an investor reports a foreign dividend representing the fair market value (FMV) of the spin-off corporation shares for Canadian income tax purposes. Also, the ACB of the spin-off corporation shares would be equal to the foreign dividend reported.

Tax planning opportunity – Section 86.1 election

Section 86.1 “Eligible distribution not included in income” of Canada’s Income Tax Act allows investors to make an election (S.86.1 election) in respect of foreign spin-offs, effectively changing the nature and timing of Canadian taxable income reported.

The S.86.1 election is available where both the original and spinoff corporation have met certain conditions, submitted the appropriate supporting documentation to the Canada Revenue Agency (CRA), and CRA in turn has approved the use of the S.86.1 election for Canadian investors.

The S.86.1 election allows an investor to exclude the distribution being reported as taxable foreign dividend, and the ACB of the spin-off shares is carved off from the ACB of the original shares. Simply, the S.86.1 election eliminates the current reporting of a foreign income receipt, taxed as regular income, and triggers an increased capital gain (or reduced capital loss) to be reported in the future when the respective original and spin-off shares are sold.

The S.86.1 election is available for investors who are an individual, a trust, or a corporation, and the spin-off distribution was reported in an open, non-registered account.

How to report an S.86.1 election?

To implement a S.86.1 election, an investor would include a letter with their income tax return for the year in which the spin-off occurs. The letter should reflect the following information:

The investor (as a taxpayer) would like to make a S.86.1 election to defer the reporting of the foreign distribution, including the names of the original and spin-off corporations.

The number, ACB, and FMV of the original corporation shares before the distribution and after the distribution.

The number, ACB and FMV of the spin-off corporation shares after the distribution.

A copy of the Statement of Investment Income (T5) slip that reflects the foreign dividend representing the distribution.

Note that if a S.86.1 election is implemented, an individual investor’s income tax return may not be electronically submitted to CRA. Corporate investors can reflect in “Notes to Financial Statements” in the GIFI section of the Corporate Income Tax Return or separately submit the letter (hard copy) to its respective Tax Centre.

** Please note that the S.86.1 election is included in the list of prescribed elections found in Section 600 of the Income Tax Regulations allowing a late, amended or cancellation of a previously filed election. The Minister of National Revenue has the discretion to grant taxpayer relief and allow late and amended elections.

Client Scenario Continued:

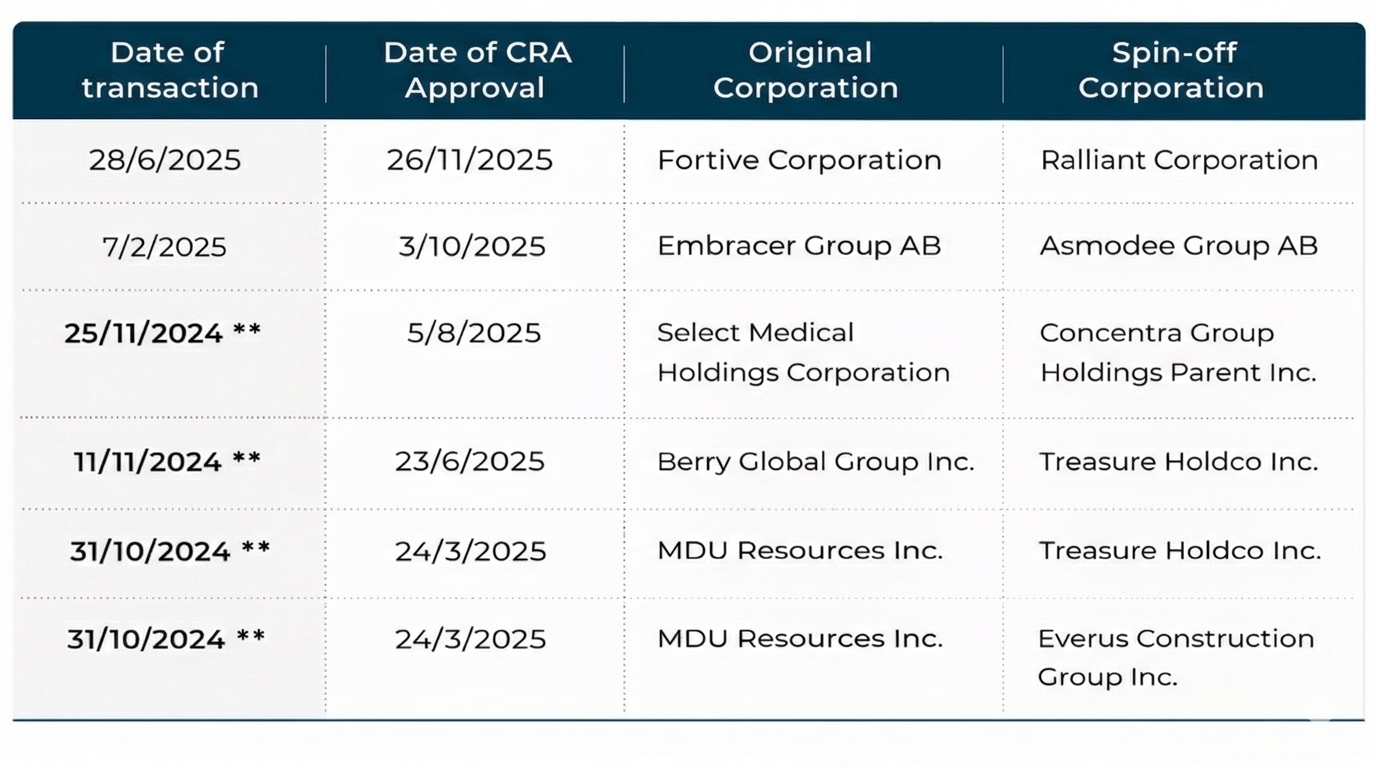

As the Fortive/Ralliant foreign spin-off was approved by CRA, Mr. Singh has two options in terms of reporting on his 2025 Canadian Income Tax and Benefit return, namely:

- Reflect the $47,000 foreign dividend as income. His Ralliant shares will also have an ACB of $47,000 going forward; or

- Elect under S.86.1 to not report the $47,000 foreign dividend and recalculate the ACB of his Fortive and Ralliant shares.

Here are the relevant details from June, 2025 Fortive’s spin-off of Ralliant needed for the S.86.1 election:

- Fortive had 339 million common shares issued and outstanding and spun off 113 million common shares of Ralliant.

- Fortive FMV after the spin-off was $17.628 billion, or approximately $52.00/share.

- Ralliant opened at $47.00/share on June 25.

- Mr. Singh owned 3,000 shares of Fortive with an ACB of $90,000 ($30.00/share).

- Mr. Singh received a foreign dividend of $47,000, and 1,000 shares of Ralliant due to the spin-off.

- Mr. Singh’s 1,000 shares of Ralliant reflected an ACB of $47,000 ($47.00/share).

Under S.86.1, Mr. Singh’s ACB for his Fortive shares will be reduced by, and his Ralliant shares ACB will determined to be, by the following formula:

= A * B / C

A = ACB of Mr. Singh’s Fortive share prior to spin-off ($30.00 USD)

B = FMV of the fraction of Ralliant share received for each Fortive share owned (1,000/3,000 * $47.00 = $15.67)

C = Sum of the FMV of a Fortive share after the distribution and the FMV of the portion for a Ralliant share received for each Fortive share ($52.00 + $15.67 = $67.67)

= A ($30.00) * B ($15.67) / C ($67.67) = $6.95 per share

Therefore, the ACB of Mr. Singh’s:

- 3,000 Fortive shares going forward are $90,000 - (3,000 * $6.95) = $69,150; and

- 1,000 Ralliant shares going forward are $6.95/(1/3) * 1,000 = $20,850.

$69,150 + $20,850 = $90,000, the original ACB of Mr. Singh’s Fortive shares.

By electing to apply S.86.1 to the Fortive/Ralliant spin-off, Mr. Singh does not have to report the $47,000 foreign dividend in 2025. As well, when he disposes of his respective Fortive and Ralliant shares in the future, he will likely generate a greater capital gain which will attract a lower income tax rate.

Connect with KLT Wealth Management

If Mr. Singh and his tax advisor decide to file the S.86.1 election for the Fortive/Ralliant spin-off, he should reach out to his wealth advisor to adjust the ACB of his Fortive and Ralliant shares on a go-forward basis.

Disclaimer

KLT Wealth Management is an owner and partner in the Q Wealth Partnership. Portfolio Management services are provided by Q Wealth. Financial planning services are provided by Camaco Capital Management. This document has been provided for information purposes only and is not intended to be relied upon as investment, financial, tax or legal advice. Please consult an independent legal or tax professional if considering the implementation of a planning strategy. The planning strategies and technical content are provided for the general guidance and benefit of our clients at the time of writing; however, we cannot guarantee the accuracy or completeness of the information contained herein.